Owning a home is a dream for millions of Pakistanis. To make this dream achievable, the Government of Pakistan in collaboration with the State Bank of Pakistan (SBP) has introduced the Mera Ghar Mera Ashiana Loan Scheme 2026. This initiative aims to provide affordable housing finance to low and middle-income families who struggle with rising real estate and construction costs.

In this article, we will break down the scheme, its benefits, limitations, application process, and the challenges it faces in today’s market.

What is Mera Ghar Mera Ashiana Loan Scheme 2026?

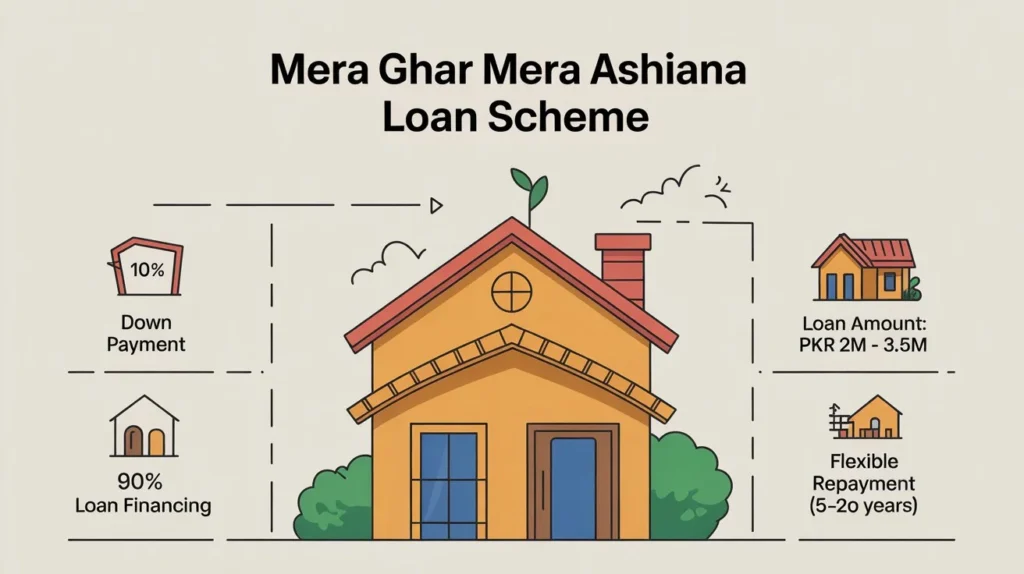

The scheme is designed to offer home financing between PKR 2 million (20 lakh) and PKR 3.5 million (35 lakh). Applicants are required to pay 10% as a down payment, while the remaining 90% is financed through the loan.

The financing can be used for:

- Purchasing a house or flat

- Constructing a home on owned land

- Financing a plot with construction plans

Features of the Scheme

- Loan Amount: PKR 2 million – PKR 3.5 million

- Down Payment: 10% of the property value

- Financing Coverage: Up to 90% of the cost

- Markup Rate: Expected between 5% – 8% (depending on loan category and bank)

- Repayment Tenure: Flexible options ranging from 5 to 20 years

- Eligible Banks: Primarily through HBFC (House Building Finance Corporation), Microfinance banks, and other scheduled banks

Who Can Apply?

The scheme is targeted at:

- Low and middle-income families

- First-time home buyers

- Individuals with verifiable income sources (salaried or self-employed)

- Applicants who do not already own a house in Pakistan

Application Process – Step by Step

- Prepare Documents

- CNIC

- Proof of income (salary slips, business statements)

- Property details (if purchasing or constructing)

- Visit a Participating Bank

- Apply at HBFC, microfinance banks, or other SBP-approved banks

- Fill Application Form

- Provide personal, financial, and property details

- Loan Approval & Verification

- Bank verifies income and property eligibility

- Disbursement

- Funds are released either directly to the builder/developer or in stages for construction

Challenges and Criticism

While the scheme looks attractive on paper, experts and stakeholders in Pakistan’s housing sector highlight several issues:

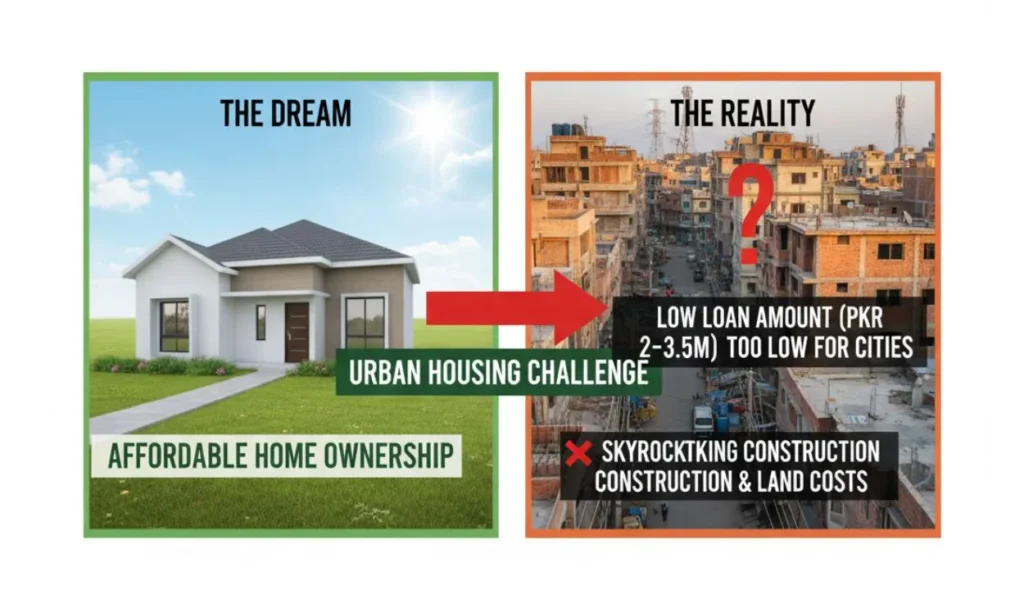

- Low Loan Amount: In major cities like Karachi, Lahore, and Islamabad, where property prices are extremely high, PKR 2–3.5 million is not enough to buy or build a home. Even small flats in urban areas often exceed PKR 10 million.

- Rising Construction Costs: With construction costs averaging PKR 6,000 per square foot, plus utility connection charges (often PKR 300,000–400,000 just for electricity meters), the allocated loan is insufficient.

- Land Prices: Beyond construction, land acquisition costs are skyrocketing, making affordability a serious challenge.

- Limited Bank Participation: Some banks hesitate to provide loans due to high default risks and policy gaps. HBFC, once a primary lender, has reportedly shifted focus toward ready properties instead of construction loans.

Real-World Impact

- Urban Housing Shortfall: Pakistan faces a housing shortfall of over 10–12 million units (World Bank estimate). This gap continues to grow each year.

- Katchi Abadis (Informal Settlements): Nearly 50% of Karachi’s population lives in informal housing, where financing options are almost non-existent.

- Middle-Class Struggles: Even middle-income families find it nearly impossible to own property in cities without substantial savings or family support.

How Does It Compare with Previous Schemes?

- Naya Pakistan Housing Scheme (2019–2021): Offered financing up to PKR 10 million with markup as low as 5% for 5 years. It was more aligned with real housing costs.

- Current Scheme (2026): Although well-intentioned, it is limited by its low financing ceiling. Experts recommend raising the loan amount to at least PKR 10 million to match today’s market realities.

Pros and Cons

Pros

- Low down payment (only 10%)

- Easy installment plans over long tenure

- Special focus on low and middle-income groups

- Support for both house purchase and construction

Cons

- Loan amount too low for metropolitan housing

- Rising construction and land costs not accounted for

- Limited reach of HBFC and microfinance banks

- Lack of strong incentives for private banks

Final Verdict

The Mera Ghar Mera Ashiana Loan Scheme 2026 is a step in the right direction for addressing Pakistan’s massive housing shortage. It provides hope to families dreaming of owning a home. However, unless the loan ceiling is increased and banks are fully engaged, the scheme may remain out of touch with ground realities—especially in big cities.

Rating: 3/5 ⭐⭐⭐ – Good initiative, but needs stronger policy backing and realistic financing limits to truly empower Pakistani families.

Key Takeaway

For many Pakistanis, this scheme may work as a starting point especially for small towns and rural areas where property prices are lower. But for urban residents, larger financing and better stakeholder collaboration are essential to turn the dream of “Mera Ghar Mera Ashiana” into reality.